09 Kasım 2024 - 13:06 - Güncelleme: 09 Kasım 2024 - 21:58

1. Introduction

Since 2018 there has been spectacular growth in marine farming of salmon trout in the Turkish Black Sea region. Despite the presence of Norwegian capital, companies, and expertise in all Atlantic salmon and salmon trout1 farming regions elsewhere in the world, there has been almost no involvement of Norwegian companies in the production of ‘Turkish salmon’ (as the salmon trout is branded by Turkish producers). This is all the more striking considering that Norwegian capital and expertise actually initiated development of Atlantic salmon farming in the Black Sea in the early 1990s. In this article I review and compare the Norwegian initiative in the 1990s with the current success to make two contributions to the literature about fish farming. The first is simply to tell the largely unknown stories of the two salmon/trout farming developments in the Black Sea: Why did the Norwegian-led initiative in the 1990s fail, and what explains the recent ‘endogenous’ success? The second is to explore what these stories can tell us about the development and character of the global salmon value chain: Atlantic salmon has been the leading species in the globalization of seafood markets since the 1980s ([31]: 3). Understanding the development and character of the global salmon value chain (GSVC) is therefore crucial for grasping the development of aquaculture value chains. Using a historical approach, I zoom in on international dynamics in a few cases where capital, expertise, fish, and governance meet and ask why Norwegian capital and businesses is not engaging in this commodity frontier? Why has farming of salmon trout in the Black Sea not become integrated into the Norwegian-dominated GSVC? What is the character of capital and its organization in these stories? To fully address these questions, I discuss not only the role of businesses and experts, but also account for the way geopolitics impacts business development and value chains, what role international organizations may have had, how other Norwegian fish farming initiatives in Turkey have played out, and how authorities in Turkey have approached fish farming.

The approach taken in this study is ethnographic, historical, and comparative. I have extensive ethnographic fieldwork experience in the region from 1990 onwards including a survey of fish farming developments in 1994 [28]. Later visits dedicated to fish farming took place in 2021, 2022, and 2023, amounting to a total of approximately six weeks of fieldwork. Meetings included leaders of several major ‘Turkish salmon’ producers, central and regional fish farming administration and research, as well as small entrepreneurs, workers, fishers and others involved in or impacted by fish farming. Additionally, in 2023 I interviewed six Norwegians who had been involved in fish farming initiatives in Turkey at some point from the late 1980s to 2016. I have also spoken to a few Norwegian actors who currently have some involvement in Turkey. I have consulted original sources in Norwegian, English, and Turkish, including policy documents, reports, news media, business media, and the like. All translations from Norwegian and Turkish are by the author.

The article proceeds by first reviewing (a) the character of the global salmon value chain, with a special emphasis on the Norwegian salmon industry, and (b) the development and status of aquaculture in Turkey. It then (c) delves into a case study of the Norwegian-led Atlantic salmon initiative in the Black Sea region in the 1990s, including a discussion of the influence of state and international institutions. This is (d) subsequently contextualized by reviewing other Norwegian involvements in fish farming in Turkey, especially a significant and successful engagement in seabass and seabream farming in the Turkish Aegean during the 2000s. The last, empirical Sections 10 and 11 discusses reasons for the recent success of ‘Turkish salmon’ and briefly outlines some characteristics of the industry. These five stories are brought together in the discussion and conclusion, where I analyse processes of emergence and change in the organization of the GSVC. The perspective from the margins or periphery of the value chain enables me to make the following arguments: there has been a general trend from an entrepreneurial to managerial approach among lead firms in the GSVC; the value chain has become more multipolar; and Turkey has moved up the value chain. Overall, the story of Atlantic salmon and salmon trout in the Black Sea shows that there is no simple expansion of Norwegian interests within the GSVC. Geopolitics and perceptions of risk have been among the variables that have kept Norwegian capital and companies out of Turkish aquaculture.

2. The global salmon value chain

Norway has since the start been the hub for capital, knowledge, technology, and production of Atlantic salmon and its close relative rainbow trout. Not only does Norway dominate salmon production (55 % of world production), but Norwegian capital, companies, and technology largely have a hegemonic position in the GSVC [6]. While production in Norway itself is part of a very globalized value chain – for instance, 92 % of feed ingredients are imported and 95 % of the salmon is exported –Norwegian interests in and control over the GSVC extends much farther; major multinational salmon corporations headquartered in Norway own and operate salmon production in every major salmon producing region in the world. Additionally, Norwegian suppliers of fish farming expertise, finance, insurance, and equipment are heavily involved in these same regions. While the character of this hegemony may have changed, Norwegian fish farming capital and experts started to seek opportunities abroad as early as the 1980s [21], [35]. Certainly, some entrepreneurs experienced limited investment opportunities at home, but the primary motive for looking outwards was the possibility of turning the edge Norwegians had in technology and know-how into profit in relatively unexplored, frontier geographies.

Salmon farming is now an extremely complex, technologically advanced, and commercially integrated industry. Innovations especially in the supplier industries allowed 'economies of scale to be exploited' ([1]: 766). Fish are highly standardized, and there is increasing focus on sustainability which is managed through standards, certification, and audits. Through company growth and expansion as well as mergers and acquisitions, the global salmon industry has become increasingly vertically and horizontally integrated. This integration started in Norway in the early 1990s; today’s structure was largely in place by 2006 [20]. A similar process took place in Chile during the 1990s [12], [32].

Fish farming in Norway and other salmon producing regions is now ‘mature’ in the sense that there is little scope for expansion. Yet, the aim of Norwegian authorities is for the sector to produce 5 billion tons by 20502 and the industry itself is eager to expand. However, “the Norwegian aquaculture industry is…hindered by formidable barriers to further growth” and “…further expansion has been limited due to stricter regulations as a result of increasing environmental and fish welfare concerns” ([2]: 3–4). Production of salmon in Norway has since 2021 stagnated at approximately 1.6 million tons. ‘The global salmon farming industry is highly constrained right now in all the major countries…growth is constrained by a myriad of factors but mostly by regulation.’3; In Norway, Maximum Allowable Biomass has since 2005 provided the overall framework on which all other regulations are based, incorporating a range of concerns and issues [22]. Among these, the spread of sea-lice is the major issue, with regulations limiting territorial expansion for the industry through the ‘traffic light system’. Furthermore, sourcing feed ingredients is becoming increasingly challenging, and worries about environmental impacts and fish welfare threaten to jeopardize the salmon industry’s social license to operate. A new controversial ground rent tax in Norway, claim the companies, slows investment in Norway and induces them to look for investment opportunities abroad. Overall, there exists in many salmon producing countries a ‘wide range of social-ecological factors limiting aquaculture expansion…, including access to suitable environments, interaction with other sectors, and policy and regulatory gaps’ ([36]: 216).

Two major strategies for expansion can be imagined ([8]: 183): The first is ‘commodity deepening’ which implies intensification through innovation and capitalization. While “the most radical innovations occurred early in the history of the industry” ([1]:766), current developments – in Norway stimulated by an innovation policy implemented through ‘development licenses’ [1] – include for example very capital-intensive development of off-shore fish farming, land-based farming in closed or semi-closed facilities, new feed ingredients, digitalization and improved monitoring and calibration of feeding and operations, as well as “deepening the market by the introduction of new product forms” ([33]: 1). Afewerki and colleagues claim that the aggregated effect of this may be the emergence of “new value chain configurations” ([1]: 766). The second is ‘commodity-widening’ which involves extensive expansion, primarily through exploring new geographies (opening new frontiers in new places). There are, however, very few geographical frontiers left to explore for salmon farming: Iceland is, according to the industry experts in IntraFish, ‘kind of one of the last frontiers for salmon farming right now’.4 Thus, it is not far-fetched to think that the Black Sea – producing more salmon trout than Atlantic salmon produced in Iceland – would be an attractive region into which Norwegian salmon capital could expand and that major Norwegian salmon producers would be in a privileged position relative to Turkish operators. That was indeed my assumption in the mid-1990s [28]. However, this was not the way things played out in Turkey: While Norwegian investment in the 1990s failed, ‘Turkish salmon’ has recently become a great success in Turkey largely without Norwegian capital and know-how.

3. Aquaculture in Turkey

Overall, development of aquaculture in Turkey parallels the global trend. While capture fisheries have declined, aquaculture production has increased consistently since the 1990s and by 2020 overtook fisheries in volume and value. Sea bass, sea bream, and white-fleshed freshwater rainbow trout each account for approximately 30 % of total aquaculture production of around 300,000 tons/year, making Turkey the second largest aquaculture nation in Europe (after Norway).

Farming of freshwater rainbow trout in Turkey started around 1970. Over the next ten years farming of portion-size rainbow trout for the local and national markets became common in the mountainous eastern Black Sea region. Still dominated by small family firms, freshwater farming of rainbow trout has continued to grow in volume and has spread to regions beyond the Black Sea. Total production started to rise significantly from the mid-1990s until approximately ten years ago and has since been a little above 100,000 tons annually, a significant portion of which is exported. With several decades of widespread farming there has thus developed robust knowledge about the practice of farming rainbow trout.

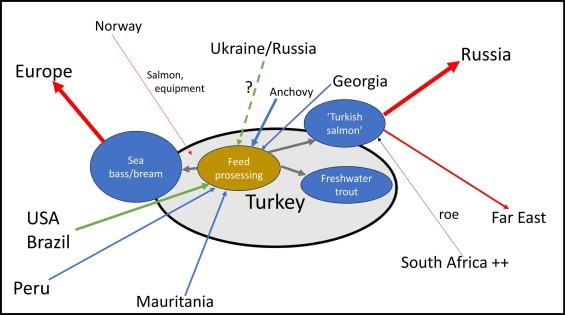

Farming of seabass and seabream (SBSB) started in the Aegean in the mid-1980s, took off in 1993, and has grown consistently since. Greece was initially the largest producer, and between 2005 and 2012, Greek fish farming companies bought heavily into the rapidly developing aquaculture sector in the Aegean region of Turkey.5 Through mergers and acquisitions, the sector was consolidated into fewer corporations, Greek as well as Turkish. But as early as 2010 it was reported that ‘because of the ongoing crisis in Greece, Turks have bought several Greek firms’,6 and eventually a few larger Turkish corporations came to dominate SBSB production in Turkey, which is now the leading producer of these species globally. Moreover, ‘the Turkish aquaculture sector…is completely self-sufficient, capable of meeting all its needs from domestic suppliers’.7 For environmental reasons, and so as not to disrupt the tourism industry and also to increase production capacity and efficiency, sea pens have increasingly been situated offshore [16]. ‘The high capital investment required for the establishment of offshore facilities (e.g. cages and sophisticated mooring systems) along with market dynamics (e.g. competition in domestic and international markets and lower profit margins) pushed the companies to consolidate and increase in scale’ (WWF 2021: 16). Turkish capital and vertically integrated companies now totally dominate the SBSB sector in Turkey [11], [16] and one firm (Kiliç Deniz) has even expanded abroad with production in Albania (for the European market) and the Dominican Republic (for the US market). SBSB production in Turkey can no longer be considered a resource frontier and is today, like the Norwegian-dominated salmon industry, consolidated and ‘mature’ with few options for expansion [16]. The largest corporations now organize most links in the value chain, from fish meal and fish oil factories in Mauritania, through feed production and fish farming in Turkey, to sales organization in Europe [11]. Fig. 1. Overview of aquaculture in Turkey with a focus on flow of fish and feeds (Red arrows: international trade of fish, blue arrows: marine ingredients, green arrows: plant ingredients).

4. Norwegian salmon in the Black Sea in the early 1990s

While on a sailing holiday in Turkey in the mid-1980s, Norwegian businessman Petter Dale, having had some success in the sale of stylish furniture in Oslo, realized that seafood was often expensive in Turkey. He started selling cheap Norwegian mackerel to Turkey – a continuing success today, though he left the business long ago. Although not involved in salmon farming in Norway himself, he saw a potential for rearing Atlantic salmon in the Black Sea. He pulled some strings and brought together capital (his own and others’) and expertise as well as a network of influence. The microbiologist, Jan Raa, at that time head of National Institute of Fisheries and Aquaculture (Fiskeriforskning) in Tromsø, Norway, was brought in to survey the natural conditions for Atlantic salmon farming in the Turkish Black Sea region. The retired Norwegian general and Chief of Defence Sverre Hamre secured contact to the very top of the Turkish state through his relations with fellow NATO officers. In 1987 the company Bio Akva AS Turkey was established with a shareholding capital of 2.67 million USD8 and 55 % Norwegian and 45 % Turkish ownership. Raa toured the Black Sea coast by helicopter together with government ministers, and overall, the initiative was met with considerable interest. National and local newspapers reported that the ‘Norwegian Professor Jan is going to give life to the Black Sea’,9 and ‘in place of the offended anchovy, new visitors are coming from the Atlantic’.10 This was in a context of the Black Sea often being spoken of as ‘dead’ since fisheries, especially the important anchovy fisheries, had collapsed (see [26]).

Ambitions were as grand as the rhetoric. The entrepreneurs saw a vast potential. They were talking about 10,000 tons annual production11 for a start. Several attractions were identified: The warm water (relative to the water in Norway) would secure much more rapid growth. The fact that the water is brackish also meant that there were no sea lice (a major problem and expense in Norwegian salmon farming). There were good conditions for hatcheries in the many small streams running into the Black Sea. Furthermore, the investment climate was favourable, workforce was cheap, and there was a good national market with high prices for quality fish. However, compared to places like Norway, Canada and Chile, there was one major challenge: a lack of secluded sites. There are almost no islands in the Black Sea, and some wide bays give only limited protection against weather and waves. Bio Akva decided to establish sea production facilities in the somewhat protected bay of Kefken in the western part of the Black Sea. A hatchery was constructed inland not very far away, in Mudurnu near Bolu. The first smolts were taken from the hatchery to the Kefken site in 1990 and the first Atlantic salmon harvested in the summer of 1991.

The sea facilities at Kefken were established by implementing an almost total technology transfer program from Norway. ‘A complete set of equipment for a 22,000 m3 sea farm was purchased in Norway and transported to Kefken island in the Black Sea where it has been mounted…’ ([18]:10). This included feed, vaccine, fry, work/feed boat, cages etc. Both Kefken and Bolu facilities were staffed by Norwegian technical personnel.

Inspired by the Norwegian initiative, there emerged a major Turkish venture into salmon farming in the Black Sea. İshak Alaton, at the time one of the leading businessmen in Turkey and owner of Alarko Holding, headquartered in Istanbul, made a major investment in Atlantic salmon farming with start-up capital of 2.2 million USD in 1991.12 Without previous experience from fishing or aquaculture, he created the company Alfarm, bought the company Beldem which already had licenses and equipment, built a hatchery in Sapanca, situated sea pens near Sinop, and established salmon processing facilities in Istanbul and ambitiously became involved in the marketing and trade of fish. Working closely with Jan Raa, they imported ‘the equipment and the smolt, as well as the technical manpower and expertise … from Norway, the home of salmon farming’.13

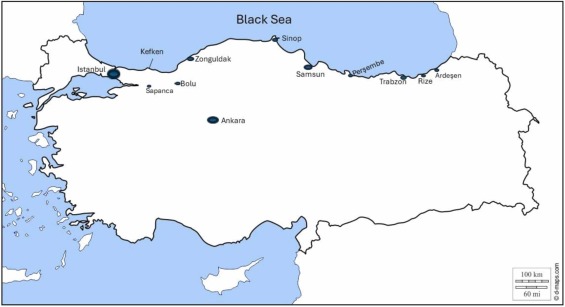

Another major Turkish investor in salmon farming in the Black Sea represented, like Alaton, ‘old capital’. Orhan Çakır, owner of the well-established fish processing plant Karsusan in Trabzon, invested 180,000 USD into Atlantic salmon and salmon trout farming in the Yomra Bay just east of Trabzon. They produced some of the feed themselves, bought the rest from a Turkish producer, imported salmon eggs, and used equipment that was both imported and locally produced. Beyond this, ‘new capital’ also contributed to boom. Among these was Can Kardeşler in Trabzon, one of the largest purse seine fishing companies in the Black Sea, which obtained license for the production of up to 2.4 million salmon, for which they received a grant of 22,400 USD. Fig. 2. Map of Turkish Black Sea region, with places mentioned in text.

5. Pumping up expectations

From the start, there was considerable media coverage of the large corporate investment in salmon, the plans and visions of Norwegian experts, and public support. In an article entitled Salmon producers, come to us in one of the major Turkish dailies, the municipal major in Ardeşen stated that ‘there is place for all here. We, as a municipality, will provide all kinds of support to all local as well as international entrepreneurs that want to invest in Ardeşen.’14 The same article also claimed that ‘according to Norwegian experts, within five years Turkey will with good planning be able to produce 30 thousand tons of salmon annually.’ Other newspaper articles ran headlines such as: ‘The salmon project took hold’; ‘Salmon provided hope’; ‘In place of anchovy, salmon fields’; ‘Freshwater trout grows bigger in seawater’ — and typically featured promises of sales and production volumes.15

The leadership at the Fisheries Research Institute in Trabzon contributed to the impression of Atlantic salmon and salmon trout farming in the Black Sea as an enticing business opportunity: ‘The aim of salmon farming is 1000 tonnes/year in 1991, in the 2000s production will reach 150,000 tonnes/year. This aim will be reached by 1000 families producing 150 tonnes of sea trout annually…and one family firm’s annual income will be 1,200,000 dollars…which is 60 times what a family gets from producing hazelnuts or tea in the Black Sea region’ ([15], quoted in [4]: 119). The director of the Fisheries Research Institute travelled along the coast presenting his visions for fish farming to ‘water produce’ cooperatives. In one such meeting which I attended in the summer of 1990, he showed videos displaying possible cage designs and explained the potential for fish farming in the Black Sea as well as what state support could be expected by prospective entrepreneurs. He mentioned the Norwegian Atlantic salmon farm in Kefken and said that he had invited experts from Norway, Finland, Sweden, Japan, France, and the US to come to a meeting at his institute to discuss fish farming.

Thus, when more than a hundred small entrepreneurs ventured into this business in the early 1990s, it was in an atmosphere of inflated expectations for the potential of fish farming in the Black Sea. By 1993, while 138 had applied to start salmon farming in the Black Sea region, 24 actually started operation.16 In the province of Trabzon, 50 applied to start farming of Atlantic salmon and/or salmon trout in the sea, of which 16 started, mostly with salmon trout. Typical licensed capacity was 200–400 tons, using circular cages with a 10 m diameter. These businesses to a large extent used locally produced equipment (e.g. cages from Armaplast in Izmit) and feed (Pinar).

6. Turkish government policy

In addition to the media coverage and the example set by the large corporations, state policies were a driving force and responsible for many local firms plunging into fish farming in the Black Sea. In Turkey, state policies towards fisheries have, since the early 1970s when responsibility for fisheries was transferred to the Ministry of Agricultural Affairs (MARA), been very ‘agriculturalist’ ([26]: 60), focusing on ‘water produce’ in place of ‘fisheries’ and aiming to increase ‘production’ in place of managing ‘fish catch’. Within this framing along with a ‘water produce’ state bureaucracy and research largely manned by agricultural engineers, aquaculture received an inordinate amount of attention. Thus, ‘water produce’ units within the MARA were more than ready to support fish farming when salmon ‘appeared on the scene’.

Direct state support for aquaculture development is difficult to chart, both as regards practices during the 1990s and the current situation. The lack of clarity stems in part from the various kinds of more generalized support provided by the state which can also benefit aquaculture. State support was certainly significant, but the scope of this article only permits a short overview and a few examples.17 Overall, government incentives included subsidized credits, tax and VAT rebates, and capital grants covering parts of investment costs.

In the early 1990s the state provided grants covering 25 % of investment costs in aquaculture through the MARA provincial offices. According to officials I spoke to in 1994, the provincial office in Trabzon paid 240,000 USD in such grants to 20 small fish-farm entrepreneurs in the Province of Trabzon, such as the grant to Can Kardeşler mentioned above. In addition, fish farmers could take loans with subsidized interest rates from the state-owned Agricultural Bank (43 % in 1994, well below current inflation). It is often claimed (see e.g. [10]: 117) that many in Trabzon and elsewhere in the Black Sea region took the investment grants and subsidized credit without ever embarking on fish farming. Officials in Trabzon admitted that it was difficult to get people to return the grant if they had not fulfilled the grant conditions.

For international capital, state policies were important beyond direct financial support. For example, during the 1980s and 1990s Chile’s emergence as an attractive investment location for salmon firms was greatly facilitated by its open economy and friendly investment climate (see e.g. [32], [12]). Turkey had seen a similar political economy evolving, with a military coup in 1982 followed by economic liberalization. This meant that setting up business in Turkey was fairly simple and attractive for foreign capital. A Norwegian sales prospectus to attract investors for a (non-realized) Atlantic salmon RAS facility in Turkey lists advantages of investing in Turkey, including there being ‘a taxation agreement between Turkey and Norway’ and ‘government incentives, such as low taxation of income, and free export of profits’ [5]. Fish farming and hatchery development were also eligible for incentives from the Directorate of Foreign Investment to attract international capital ([19]:175).

7. International institutions and geopolitics

International institutions have also promoted the development of aquaculture in the Black Sea region of Turkey, especially during the early 1990s. What was the effect of these initiatives? In 1990 Turkey was in many respects considered a developing economy in need of support. At the same time, aquaculture had emerged globally as a promising new economy worthy of development assistance. For instance, the Japan International Cooperation Agency (JICA) held a central role in the development of salmon farming in Chile from the late 1960s to the late 1980s. This included facilitation of access to the Japanese market [23]. The Canadian International Development Agency also played some role in the development of salmon farming firms in Chile [12]. While international institutions may have been inspired by the emerging SBSB farming in the Turkish Aegean and the promise of salmon farming in the Black Sea, the ecological/fishery collapse in the Black Sea together with the new geopolitical situation with the disintegration of the USSR made their involvement more relevant and desirable. While the UN-FAO had hitherto been the major external supporter of fisheries research and development, including a 1979 mission on the development of aquaculture in the Black Sea [34], the World Bank became a more important player after 1990. In 1993 MARA commissioned several extensive reports on aquaculture development in Turkey. The work was funded by the World Bank and a Japanese grant and undertaken by the UK consultancy firm MacAlister Elliott and Partners Ltd. [14], [30], who advised that the authorities should encourage marine aquaculture other than Atlantic salmon and salmon trout. In a development probably independent of the WB-funded studies, the WB agreed in the early 1990s to provide a 30–40 million NOK loan on favourable conditions (3 years, instalment-free, with interest well below inflation) to an ambitious BioAkva offshoot that planned to farm Atlantic salmon in large floating tanks with cold flow-through water from below the thermocline. The plan stranded only on the major Norwegian owner’s hesitance to allow the Turkish partners to have influence in the joint venture.

In a parallel development, the Global Environmental Facility (funded by UN organizations and the World Bank) established the Black Sea Environmental Programme (BSEP) in 1993 with the aim ‘to provide a sustainable basis for managing the Black Sea’ [19]. BSEP facilitated a range of studies and initiatives, including a comprehensive survey and scoping study of aquaculture in all Black Sea countries in 1994 (ibid.). The ToR for the aquaculture study mission notes the ‘rapid decline in the Black Sea capture fisheries’ and identifies aquaculture as a possible alternative to generate income in the region. In the Turkish leg of the survey ([19]: 169–180), again conducted partly by MacAlister Elliott and Partners Ltd. in close cooperation with personnel from the MARA, the mission focused primarily on the status of and reasons for failure in marine farming of Atlantic salmon and salmon trout, detailing technical, biological and market challenges, without providing any clear recommendations.

A third development in this period was JICA’s support for and cooperation with the state Marine Research Institute in Trabzon concerning breeding and farming of turbot, a species heavily decimated by fishing and other pressures. Turkish authorities took the initiative in 1994 and the project ran from 1997–2007. The ambition was to achieve something similar with turbot in Turkey as JICA had achieved with salmon in Chile; although technically largely successful, commercialization proved difficult.

Finally, from 2003 onwards, fisheries were included as a separate item in the twinning processes to align Turkish legal structures with those of EU. Aquaculture was incorporated in the comprehensive review of the ‘water produce sector’, which noted that a ‘weak variable’ ‘on the topic of dissemination of aquaculture was the lack of strategic control’ ([17]: 11). However, actual measures taken during the twinning process largely addressed fisheries (port offices, vessel tracking system, etc.). Anticipated legal changes to secure alignment with the acquis (the body of common rights and obligations that is binding on all the EU member states) would have had implications for aquaculture, but legal and regulatory changes were minimal before negotiations of the Fisheries Chapter were frozen (by the EU) as early as December 2006. More recently the EU funded, through its European Neighbourhood Instrument, a comprehensive study of aquaculture in the Black Sea region (excluding Bulgaria and Russia but including Greece) [13]. Although the intention of this project has been to promote the sharing of ‘good practice’ in aquaculture, it seems to have had little impact on developments in Turkey.

Despite the interest and effort international institutions showed, they did not really have much impact on the actual development of fish farming in the Turkish Black Sea region, in part because political and economic developments hampered implementation or made them irrelevant. MacAlister and Elliot was initially brought in to help assess suitable locations for fish farming in the coastal Black Sea, but management in MARA found their recommendations unrealistic since the report considered almost all coves, bays and lagoons suitable for fish farming. Elements of later reports by MacAlister and Elliot were incorporated to some degree in the national five-year development plans, but sparsely implemented due to the economic crisis in Turkey during 1997–2001. Thus, except for JICA, international initiatives were not followed up by funds or activities. Even before the occupation of Crimea in 2014, relations with Russia had become very strained; there was no longer hope for the Black Sea becoming an integrated political-economic area [27]. Without political and economic support, the BSEP withered. At the same time, Turkey drifted further away from the EU while it developed a stronger export-oriented (but debt-financed) economy. When the ‘Turkish salmon’ sector finally took off around 2018, international institutions played no significant role.

8. Salmon collapse

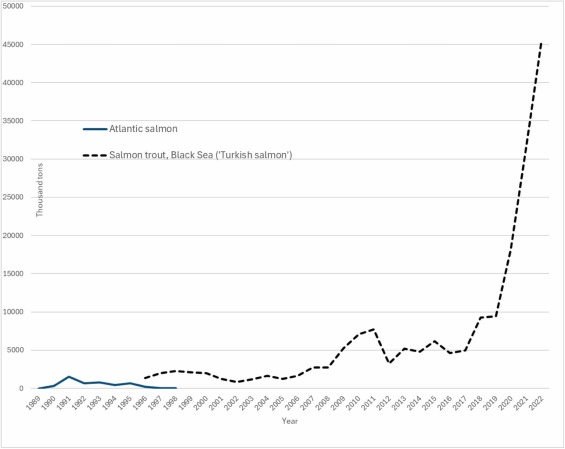

Despite the promise of Norwegian technology and expertise, the investments of the Turkish state, and the extensive survey and research by international organizations, the salmon adventure in the Black Sea failed. When I visited in 1994, the three largest salmon firms reported profits and expressed high expectations and ambitious plans. The smaller local ones, focusing largely on salmon trout, had all but given up. In 1994 there remained only nine small companies farming salmon in the provinces Trabzon and Rize, typically operating a few small cages within (artificial) harbours (to be protected from strong weather/seas).18 It was this divergence between large and small which informed my expectation [28] that capital and Norwegian technology/know-how was required to succeed. However, by 1996 the whole sector (Atlantic salmon, salmon trout), both small and big companies, except for a few very small local producers, had collapsed. The adventure had ended (See Fig. 3). Fig. 3. Production of Atlantic salmon and salmon trout, Turkish Black Sea 1990–2022. Source TUİK. Preliminary figures indicate salmon trout production of approximately 90,000 tons in 2023 and an expected 85,000 tons for 2024.

Can Kardeşler had problems mooring the cages which were then destroyed in winter storms, allowing fish to escape. Marketing the fish was also difficult. So, in the end, they operated only for a year or two. Karsusan also discontinued their fish farming activities. BioAkva went bankrupt and its Norwegian employees left Turkey. Alfarm sold the remains of their equipment to a local entrepreneur but continued processing and selling Atlantic salmon – imported from Norway.

What caused the collapse? For one, harsh winter storms and strong sea currents destroyed cages, even in the partly protected bays. However, the major problem seems to have been a combination of fish mortality and marketing. Salmonides are cold-water species dependent on water saturated with oxygen. During summer, waters in the Black Sea can reach 28°C, but even at 20–22°C oxygen saturation drops to levels where the salmon easily develop fatal sicknesses. Some companies tried – with limited success – to ameliorate this with vaccines developed by Norwegian experts, but the most widespread strategy was to slaughter the salmon before summer. This meant, however, that the way challenges at the point of production were handled resulted in marketing coming up against bottlenecks of exchange: salmon flooded the market, resulting in very low prices. In Turkey, consumers have a strong preference for fresh fish [25], so freezing the salmon was not considered an alternative.

9. Other Norwegian interests in fish farming in Turkey

9.1. Black Sea flow-through

Already in the early 1990s, experience with problems created by high summer temperatures in the Black Sea led experts associated with BioAkva to develop innovative designs. In addition, the construction of large floating tanks with cold flow-through water, mentioned above, a land-based ‘run-through’ facility for Atlantic salmon farming at Kefken was designed in Norway. The project was highly ambitious: ‘this will be the largest farm in the world, either sea or land based’ ([5]: 38) and fully developed was estimated to require an investment of 15 million USD. It eventually failed to secure sufficient funding and was never realized. However, the idea lingered, and some of the same Norwegians made a new effort to establish a land-based flow-through facility west of Sinop. This only stranded when the major Norwegian investor backed out in 2016 since he considered that terror incidents in 2015 and the attempted coup in 2016 had made Turkey too risky a place to invest.

9.2. Aegean SBSB

While Norwegian capital and expertise failed in the Black Sea, it had a central role in the development of SBSB fish farming development in Turkey. This started in 1993 and was consolidated when Fjord Marine bought heavily into the industry in 2000/2001. Fjord Marine was initially part of the large Norwegian aquaculture firm, Fjord Seafood ASA, but soon became an independent firm with operations in both Norway and Turkey.19 While Paul Birger Torgnes, for decades a major player in Norwegian fish farming, had a controlling share of Fjord Marine, NORFUND, the state-owned Norwegian Investment Fund for developing countries, owned up to 30 % and two Saudi seafood corporations held most of the remaining shares.

Reidulf Juliussen, head of Fjord Marine in Turkey, found that ‘technology related to production of these species is more or less a copy of sea-based farming of salmon’.20 Norwegian expertise was central to the development of SBSB farming in several south European countries besides Turkey.21 This was part of a trend of Norwegian investment that saw consultants move into new territories and species during the 1980s and 1990s [21]. Fjord Marine in Turkey primarily imported equipment and feed from Norway but also from Greece. Through 2002–2005, Fjord Marine expanded significantly in Turkey. By 2005 they produced 5000 tons, made good profits22 and had become Turkey’s second largest fish farming company after the Turkish company Kiliç Deniz.23 At this point the Turkish operations accounted for roughly ¾ of the turnover of Fjord Marine.24

However, Fjord Marine had been running their cod farms in Norway at a deficit for several years, and after 2005, SBSB production in Turkey was no longer as profitable. The Norwegian owner had become heavily indebted to banks25 and potential investors in Norway found Turkey to be an increasingly risky place to invest for several reasons, including: hyperinflation, potential trade restrictions to be imposed on Turkey by the EU, and non-conformity with rules of impartiality as well as corruption. When Fjord Marine started to ‘think big’ about a large Mediterranean SBSB agglomeration, they had to seek for new investors elsewhere.

In Norway, Fjord Marine’s former parent company, Fjord Seafood, had been engulfed in the dramatic mergers and acquisitions that took place between approximately 2000 and 2006, and which resulted in Pan Fish buying Fjord Seafood (and Marine Harvest) in 2006, forming the world’s largest salmon corporation, now known as MOWI. The same drivers were at work in the Mediterranean as well. Informed and inspired by processes in Norway and facilitated by financial advisory services/investment banks, Fjord Marine worked in 2008–2010 together with partners in Greece, Italy, France, and Spain to make structural changes that could consolidate their activities into a much larger multinational corporation. This initiative, nicknamed ‘Big Fish’, almost succeeded, but when eventually it was clear that it would not, Torgsnes sold his shares in Fjord Marine.26

This opened the way for the Greek fish farming giant, Selonda, with its ambition ‘to hold half of all production of seabass and seabream in Europe and Turkey’,27 to buy a 46 % stake (including all of NORFUND’s shares28) in Fjord Marine. By 2012 they had full control of the company.29 However, Greek seafood companies were engulfed in the Greek debt and financial crisis and by 2013 their values plummeted; Selonda was now valued at a meagre 10.5 million Euro30 (as compared to 115 million Euro in 200731). Selonda’s interests in Turkey were likely acquired by Turkish companies.

9.3. Other steps in the value chain

Norwegian companies have some presence in Turkey related to other links in the value chain. Lerøy Seafood bought Alfarm’s processing facilities. Later MOWI also set up a subsidiary in Turkey which, like Lerøy, imports and processes Atlantic salmon from Norway. Norwegian companies continue to deliver equipment to Turkish SBSB aquaculture, and two large companies headquartered in Norway have established subsidiary firms for feed production (Skretting) and net/cage/equipment production (AkvaGroup) in the Aegean region of Turkey. In 2023 ScaleAQ, another major Norwegian equipment supplier, headed a mission of Norwegian suppliers to meet producers in the Black Sea region. After Fjord Marine pulled out and BioAkva failed, Norwegian interests have not, however, been involved on the production side of fish farming in Turkey.

10. Recent success with ‘Turkish salmon’

From approximately 2010, a few ‘Turkish salmon’ firms based in the Black Sea region32 started to grow until the sector boomed from 2018 onwards. What had changed since the mid-1990s that made farming of salmon trout a success?

First, Turkish SBSB farming along the Aegean coast had developed and matured. Technology and know-how could fairly easily be transferred to the Black Sea. This included cages designed to withstand offshore conditions much better than those used for salmon farming in the Black Sea in the 1990s as well as higher quality feeds, all produced at relatively low cost in Turkey. This made it possible to quickly scale up farming of salmon trout. Second, farming of freshwater rainbow trout had also progressed as firms gained experience with and knowledge of the production cycle of the fish. The on-land part of the production process had become stabilized. Third, a few local entrepreneurs continued experimenting with small-scale sea farming of salmon trout, especially in the protected bay in Perşembe, often in combination with farming of sea bass. Fourth, around 2000, some fish farmers started experimenting with -grow out in large dams in the Black Sea region created by hydroelectrical power projects (HPP). With accelerated development of HPPs after 2000, many new dams became available for this purpose. This created a new production cycle whereby the fish are first transferred from hatcheries to dams where during the summer they grow to 0.3–1 kg before being transferred to sea pens in the autumn. During six months in sea cages, fish are fed to grow to 3–5 kg and gain a deep red colour, before being slaughtered in April-June. Sea cages then remain fallow for almost half of the year (if not stocked by sea bass). Some fish is harvested and sold directly from the dams.

Fifth, in addition to the four production-related variables reviewed above – and of no less importance – were developments on the market side. As a retaliatory measure after Norway imposed sanctions on Russia in reaction to the invasion of Crimea in 2014, Russia banned Norwegian Atlantic salmon and salmon trout from the Russian market. Before this, Russia was the third largest importer of Norwegian salmon, in 2010 amounting to 85,000 tons, and together with Japan the most important market for salmon trout. Pioneered by Kuzoğlu, a company from Ardeşen, relations were established first to importers in Russia, later to Japan and some markets in Southeast Asia. Today almost all ‘Turkish salmon’ is exported, a significant part to Japan but 60 % of it to Russia (28,500 tons in 2022), in 2023, valuing 376 million USD. Both the Russian and Japanese market value the deep red flesh of salmon trout ([29]: 169) and producers of ‘Turkish salmon’ very much emphasize its colour when marketing the fish. Lead companies as well as regional business associations continue to try to expand the market towards Europa and China with difficulty. After the Russian invasion of Ukraine, Turkey has maintained open trade relations with Russia, but the dependence on the Russian market became evident when demand for ‘Turkish salmon’ was impacted by the Russian war-economy: In 2023 producers were unable to sell all of their produce and huge stocks (I have heard 33,000 tons) of frozen salmon trout piled up in freezing facilities along the Black Sea coast.

Sixth, state policies towards the sector strongly emphasize fast production growth and export. MARA has therefore simplified application processes, e.g. by having a less rigorous EIA process for licenses below 1000 tons, by making investment in the sector attractive by requiring only a small rent for hire of locations, and by providing financial support. While there is little direct financial support for production, there is more for investment, especially in processing facilities. A case in point is state support for a new 20 million USD investment in a fish feed factory being constructed by Black Sea Aqua Feed Group in an organized industrial zone in Samsun. This joint venture initiative by three Eastern Black Sea seafood companies, all involved in several stages of the ‘salmon trout value chain, is granted ‘[i]nterest rate support, customs tax exemption, VAT exception, support for social insurance expenses, 80 % tax rebate, investment share support 40 %’.33 These are surely very significant concessions that substantially ease capital needs and reduce risk. State support is not the major driver behind the recent growth in farming of salmon trout (in the early 1990s the sector collapsed despite significant state support) but it does facilitate rapid growth.

11. Characteristics of the ‘Turkish salmon’ sector

The Turkish salmon trout sector is now characterized by vertical and national integration, as well as leadership by few (10−15) large firms. All capital is Turkish, and all firms are family-owned and managed. The two largest Turkish SBSB firms, Kiliç Deniz and Gümüşdoğa, together with a couple of other SBSB or seafood firms based in Western Turkey have produced salmon trout in the Black Sea from 2023 and 2020, respectively. Conversely, several of the largest Black Sea firms have invested in activities elsewhere in Turkey, be it SBSB or mussel farming in the Aegean, processing in Izmir, or freshwater trout farming at different locations around Turkey. Aquaculture capital in Turkey is becoming one national sector, with the large corporations not limited to one species or region.

Although significant horizontal integration has yet to take place among the Black Sea based producers of salmon trout, actors expect acquisitions and mergers. Vertical integration is more pronounced. Most larger producers aim to establish their own feed production, all have processing and freezing facilities and manage transportation, logistics, and marketing themselves. Most have cages both in the sea and in freshwater dams, possess work/well-boats, and operate their own hatcheries. A few produce fish eggs, some have facilities for smoking salmon, and a few are involved in purse seine fisheries and related processing of fish meal and fish oil.34 A distinct characteristic of the Turkish salmon trout industry has been its relative ignorance of sustainability standards and certification programs which seem not to be requested in the markets in Russia and the Far East. The ‘Turkish salmon’ industry thus has not engaged the international cooperation relating to ‘environmental improvement and certification’ which is considered important in the integration of the GSVC ([6]: 379). This is distinctly different from the Turkish SBSB sector which early on adopted ‘EU quality standards related to fish welfare and fish safety’ ([16]: 16). While many locations producing SBSB have been ASC-certified for many years, most producers of salmon trout have only during the last year started the process to gain ASC or other certificates to improve their chance to sell to the European market.

Regulations have not restricted concentration of capital and vertical integration, quite the contrary. The state took the same approach when the SBSB sector developed, but the tools were slightly different [16]. Licensing criteria and processes for salmon trout are designed in such a way that they tend to privilege larger operators, e.g. by stipulating that the license owner shall also have or develop the capacity to process the fish produced according to the license, in effect raising the bar for how much capital is required to enter the business.

12. Discussion

The unsuccessful attempt to start farming of Atlantic salmon in the Black Sea in the early 1990s was not solely or simply a Norwegian failure. The Norwegian salmon initiative prompted a wider development in Turkey that involved old capital (Alarko), small local entrepreneurs, international organizations as well as state bureaucracy and research. One interpretation of what happened is to say that there was a ‘perfect match’, articulated in print media, between on the one hand hubristic Norwegian capital and expertise, and on the other hand a ministry with an agriculturalist approach to ‘water produce’ thinking its long-time dream of aquaculture development in the Black Sea would come true. Without this constellation the story might have been very different. But in the specific situation of the time, challenges were downplayed and the models invested in premature.35 While it is not unusual that there are expectations for salmon aquaculture resulting in local development and employment (see e.g. [24]), the way this unfolded in the Turkish Black Sea region in the early 1990s shows that it is not necessarily the industry that works the pumps.

I had thought that the accumulated expertise that put Norway in the lead internationally would make it more difficult for poor and peripheral areas, like Turkey, to develop the business independently. ‘The investments, risks and operating costs in ‘Norwegian-style’ aquaculture in Turkey can only be carried by companies with considerable financial strength’ ([28]: 5) from either foreign capital (like BioAkva) or old Turkish capital (like Alarko). I was wrong. What happened with ‘Turkish salmon’ was the opposite: Local entrepreneurs – family firms often with some prior investments and relevant experience in related sectors – succeeded through trial and error and gradual expansion. Economies of scale were (initially) unnecessary to succeed with ‘Turkish salmon’. Thus, both the 1990s failure and the more recent success with salmon trout demonstrate that in charting developments and characteristics of GVC, it is important to account for local-level processes ([32]: 120, [7]).

There is, though, a crucial difference between the early 1990s and the current-day situation in terms of the organization of the salmon farming industry. While the salmon value chain is today largely controlled by a few multinational lead firms [6], in 1990 there were no lead companies that organized significant sections of the GSVC. One may even argue that salmon was not yet organized as a GVC ([3]: 2439). In the 1980s and early 1990s, Norwegian fish farming expanded abroad to geographies suitable for farming Atlantic salmon and salmon trout but also became involved in farming of other fish species in a variety of places around the world [21]. Norwegian marine aquaculture was technologically a world leader, and in the 1980s Norwegians established themselves as expert consultants, operated farms in joint ventures [35], and went on a shopping spree of fish farming start-ups around the world ([21]: 315). Norwegian expertise was sought by local firms, as happened in Turkey (Alarko). However, when it came to capital and organization, Norwegian fish farming was still ‘entrepreneurial’ – it was largely not driven by corporate capital.

Corporate growth in fish farming in Norway was restricted by regulations that stipulated that a firm could be majority owner in only one license. Thus, in Norway the salmon industry was not organized into vertically and horizontally integrated large corporations listed on and acquiring capital on the stock market until license regulation was liberalized in 1991. When Norwegian know-how and technology were put to work in pristine waters, it was not led by large salmon corporations, but often by networks of individual experts and investors (BioAkva is a case in point) who saw the potential for turning Norwegian expertise in fish farming into profit in new places. There also emerged a few larger Norwegian firms pioneering fish farming abroad, but these were formed by parent companies whose main activity lay outside of fish farming, such as Hydro seafood (Norsk Hydro – metals, fertilizer, oil and gas), Stoltz Seafarm (Stoltz-Nilsen – shipping), and Noraqua (Selmer Sande – construction). Capital was often provided by Norwegian banks [21] or private investments and sometimes by celebrity investors ([21]: 324). BioAkva and the first Norwegian adventures into SBSB in the Turkish Aegean in the 1990s fit this picture: they were entrepreneurial, their biggest assets were Norwegian expertise, technology, and capital. When BioAkva developed their project in Turkey, they focused primarily on the production side of the value chain and paid less attention to processing and marketing. The failure of BioAkva was not unique. Some Norwegian investments, especially in Iceland and Canada in the latter half of the 1980s, led to huge losses [21].

The organization and perspective of the salmon industry have of course changed much since then. In 2024 I spoke to a representative from one of the larger salmon firms headquartered in Norway about the potential for investing in fish farming in Turkey. He was hesitant due to economic and political risk but told me they were still considering buying an SBSB firm in Turkey. He stressed that he found the company attractive precisely because ‘they have everything, including feed production, every link in the value chain’.36 While that sort of language or deliberation was not even relevant in 1990, today ‘value chain’ has become ubiquitous in corporate thinking. The visions and strategies of Norwegian salmon farming corporations extend far beyond production, and corporate governance includes rigorous risk assessments that take into consideration the whole value chain.

The story of Fjord Marine SBSB farming in the Aegean shows that it was indeed possible to succeed with Norwegian technology and expertise in Turkey during the 1990s and 2000s. However, SBSB farming was already developing when the Norwegians arrived – the business case had already been proven. With the recent success of Turkish salmon trout, its business case proven, one would expect the large Norway-based multinational salmon corporations, eager to expand into new frontiers, to enter this rapidly developing sector. And they would be very welcome: Relevant core personnel in MARA as well as fish farmers in the Black Sea region express a desire to partner with Norwegian companies so that they can improve production and processing techniques. However, except for suppliers of equipment and feed, Norwegian companies seem to be uninterested. While production of salmon trout in the Black Sea may be enticing, the larger value chain through which the fish flows may be considered vulnerable with reputational, biological, and economic risks, as partly confirmed by the 2023 market problems. Decision-makers in Norwegian salmon corporations consider Turkey a risky place in which to make long-term investments. This is part of a wider trend whereby Norwegian capital and institutions, starting around 2015, recategorized the risk profile of Turkey. The hydropower company, Statkraft, owned by the Norwegian state, put new investments on hold in 2015; the Norwegian public business promotion bureau, Innovation Norway, pulled out of Turkey in 2017; and the Norwegian Seafood Counsel followed suit, noting that ‘the political development in Turkey has played a role’.37

13. Conclusion

While a particular constellation of variables contributed to the boom-and-bust character of the Norwegian-led salmon adventure in the Black Sea in the early 1990s, the Norwegian initiative was also very entrepreneurial, high-risk, and focused on production, thus distinctly different from the approach of today’s large, vertically integrated salmon corporations with professional organizations that coordinate most stages in the salmon value chain. In the meantime, a new value chain has been forged for ‘Turkish salmon’ which is mostly independent from the Norwegian-dominated GSVC, and Turkish capital has taken increasing control over the existing value chains of SBSB. Thus, unlike the early 1990s when fish farming in the Black Sea region of Turkey was considered in need of international assistance (World Bank, BSEP) or technology and know-how transfer (primarily from Norway) to develop, the Turkish salmon trout industry is today largely self-sufficient. Developments in SBSB and ‘Turkish salmon’ farming, now nationally integrated, have been led by rapidly expanding Turkish capital – a general trend in the Turkish economy, especially after 2001. Thus, Turkish aquaculture can be said to have been moving up the value chain by acquiring more advanced capabilities and greater control of the value chain.

The empirical stories told here also demonstrate the necessity in analysis of GVC of natural resources to account for local level dynamics, historical development and change, national political economy and regulations, as well as the ecological dimension (cf. [3]). Beyond these variables, this study shows that geopolitics (important in this case) and international organizations (less important here) can impact how GVCs emerge and are organized – GVCs ‘exist within continually evolving sociopolitical environs’ ([9]: 418). That ‘Turkish salmon’ primarily serves a very particular market (Russia) makes the global salmon-trout value chain ‘multi-polar’ but in a way that cuts across the North-South divide outlined by Bush and colleagues (2019). With globalization not only reshaped but in decline, we may see more partial disjunction within what we have hitherto considered global value chains.

The authors declare the following financial interests/personal relationships which may be considered as potential competing interests. Stale Knudsen reports financial support was provided by University of Bergen. Stale Knudsen reports a relationship with University of Bergen that includes: employment and travel reimbursement. If there are other authors, they declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Acknowledgements

Fieldwork in 1994 was supported by a grant from the Agder University College, while more recent fieldworks were made possible by support from the University of Bergen. I am grateful to all individuals in Norway and Turkey whom I have interacted with in the course of this research. I am especially grateful for the support provided by Muharrem Aksungur, coordinator of the Fisheries and Water Produce section at The General Directorate of Agricultural Research and Policies, Republic of Türkiye Ministry of Agriculture and Forestry.

Data availability

Some of the data used is based on ethnographic fieldwork and interviews and is therefore of a confidential nature. Other data, such as reports and newspaper articles, can be made available on request.

Global productive capital mobility: The case of Chilean farmed Atlantic salmon

A. Boanno, J.S.B. Cavalcanti (Eds.), Globalization and the time-space reorganization: Capital mobility in agriculture and food in the americas, 17, Emerald Publishing Ltd, Cambridge USA (2011), pp. 167-204

Fisheries Acquis Centre. (2007). Su ürünleri ve yetiştiriciliği sektör çalışması nihai rapor. Ankara: Fisheries Acquis Centre. Agrotec, Tragsatec, Nautilus Consultants, KoçSistem.

Fiskeriforskning. (1992). Bio Aqua International A/S. A company engaged in the production, processing and marketing of salmon in Turkey. Tromsø: Norwegian Institute of Fisheries and Aquaculture Lt., Centre of Aquaculture Research.

GEF-BSEP. (1996). Marine aquaculture in the Black Sea region. Current status and development options (UNDP Ed. Vol. 2). New York: Global Environmental Facility.

Knudsen, S. (2015). 'Marine Governance in the Black Sea'. In M. Gilek and K. Kern (eds.) Governing Europe’s Marine Environment. Europeanization of Regional Seas or Regionalization of EU Policies? Ashgate, 225-248.

Knudsen, S. (1995). Introduction of aquaculture along Turkey's Black Sea coast: Entrepreneurs, knowledge and regulations. Paper presented at the Fifth Annual Common Property Conference, Bodø.

There are two distinct production systems of rainbow trout: portion-sized and white fleshed freshwater trout, and large, red-fleshed ‘salmon trout’ that grows big in saltwater pens. The production cycles and technology of Atlantic salmon and salmon trout farming are very similar, and 'salmon trout is well integrated into the salmon market' (Landazuri-Tveteraas et al. 2021: 169).

The large Mediterranean consortium finally came to being, of a sort, with the formation of Greek-Spanish Avramar in 2021, owned by two private equity investment firm based in New York and UAE respectively (the CEO of Avramar is, however, a Norwegian citizen). This corporation controls 70 % of Greek production of seabass and seabream, but Greek fish farming now lags significantly behind Turkey in terms of production and productivity.

Some of the major local firms driving this development were Kızılırmak, Omega 61, Polifish, and Kuzoğlu/Lazom. None of these were initially involved in farming of SBSB.

For a detailed description of one company integrated over the whole value chain and across regions in Turkey, see an article about the company Sürsan: ‘Full integration offers many advantages’, Eurofish Magazine 6/2021, p. 4243.

Around 1990 a more established Norwegian salmon company also considered investing in Atlantic salmon production in the Black Sea. But after a thorough review (using Norwegian experts other than BioAkva), they decided it was not worth taking the risk since the ‘hydrological conditions were not favourable’ (i.e. high summer temperatures, an exposed coast).

YORUMLAR